Max Life Smart Wealth Plan

In life, nothing gives more pleasure than seeing your loved ones fulfill their dreams, while you watch over them. As the breadwinner of the family, you work towards maximizing your savings to support your children’s education, their marriages, and your peaceful retirement. However, in today’s environment, which is full of uncertainty and volatility, you need guaranteed assurance that surmounts all such risks.

Term Insurance and Investment Plans

Tax Savings upto Rs 46,800##

Tax Savings upto Rs 46,800## 99.51% Death Claim Paid Ratio^

99.51% Death Claim Paid Ratio^ Zero Commission#~

Zero Commission#~

Zero Commission#~

Pay 16.6k monthly,Get 1 Crore

3Lacs premium back

Midcap Index Fund

Pay 10k p.m Get 1 Crore^~

Get 25.7k/Month for 25 Years

Create Wealth for Your Family’s Future Goals

With Max Life Investment Plans

Pay ₹10,000/month for 10 years

Get ₹35 Lakh*

after 20 years

100% Guaranteed returns*#

100% Guaranteed returns*# Save tax up to Rs. 46,800##

Save tax up to Rs. 46,800##

*Disclaimer : Max Life Smart Wealth Plan | A Non-Linked, Non-Participating, Individual Life Insurance Savings Plan | @₹35,26,176 as lump sum at the end of 20 years, for a 30 years old healthy male. Premium payable per month is exclusive of GST.

What is Max Life Smart Wealth Plan?

At Max Life Insurance, we understand the significance of such milestones in your Life. Thus, presenting Max Life Smart Wealth Plan (a Non-Linked, Non-Participating, Individual, Life Insurance Savings plan, UIN: 104N116V11), which is designed to help secure your financial future through guaranteed returns. This plan will help you pursue your dreams and accomplish all milestones that you set your heart on, with certainty.

Who Should Invest in Max Life Smart Wealth Plan?

Max Life Smart Wealth Plan is suitable for the following categories:

1) Salaried individuals

2) Self-employed individuals

3) People with dependents who seek a long-term financial plan

4) People who have less risk appetite

5) People who seek guaranteed returns on savings

6) People who look for dual benefits of life insurance and savings

You can buy Max Life Smart Wealth Plan to secure your retirement, for your children’s education, your spouse’s financial independence in your absence, or any other financial goals. Furthermore, this savings plan is also suitable for those investors who wish to put their money into a financial instrument, which provides long term capital appreciation, but with less risk than pure equity market investments.

How Does Max Life Smart Wealth Plan Work?

Max Life Smart Wealth Plan comes in four variants and you can choose the one which best suits your savings need. Here is how you can invest in Max Life Smart Wealth Plan:

Step 1: Choose a suitable variant

Max Life Smart Wealth Plan offers the following plan variants:

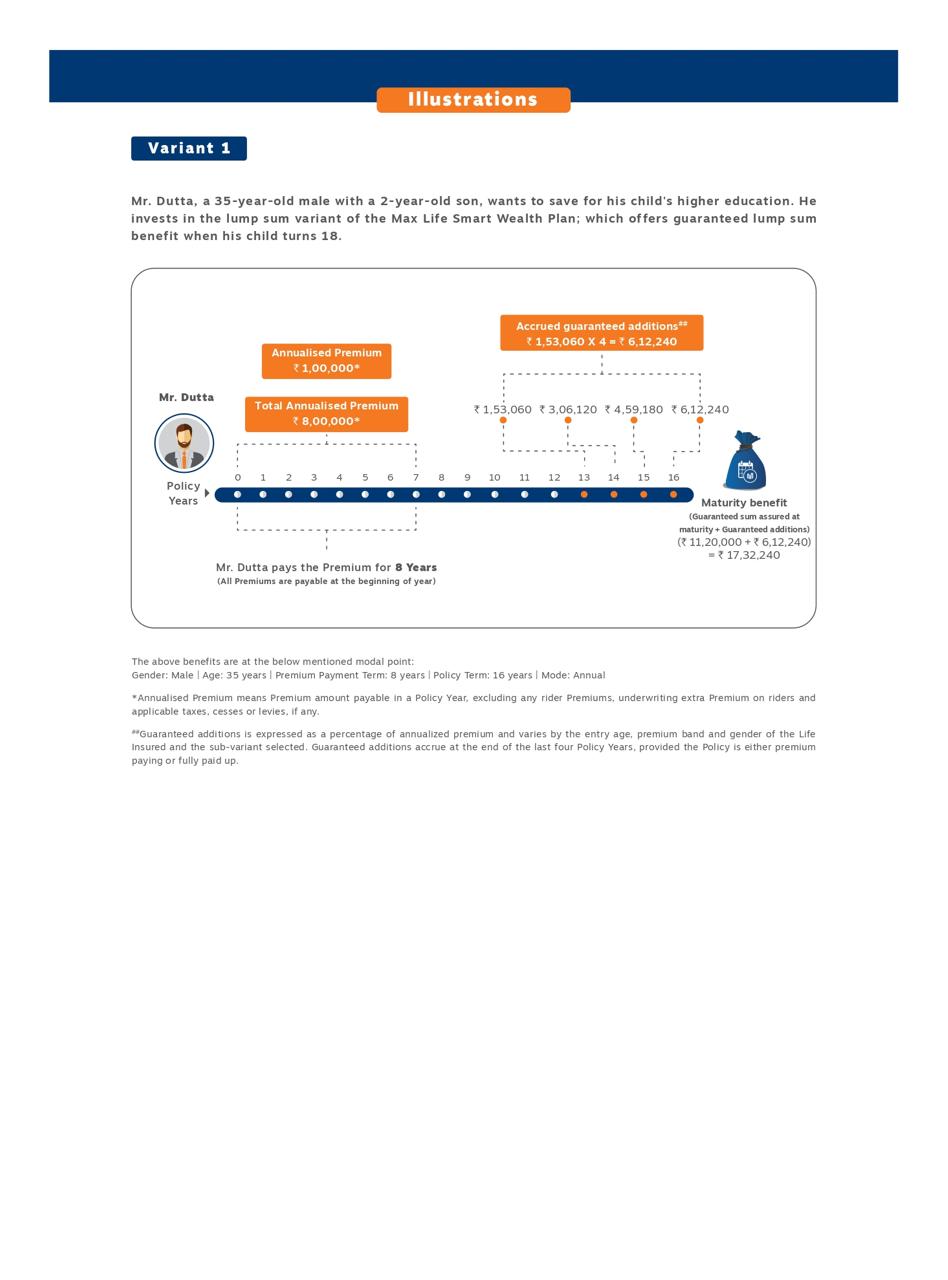

1) Lumpsum

This variant offers to pay maturity benefit as a lump sum at the end of the policy term. The maturity benefit paid comprises both guaranteed sum assured on maturity and the accrued guaranteed additions (if any). Under this variant, the Guaranteed Additions are expressed as a percentage of annualized premiums, and they may vary based on the entry age, premium band, and gender of the Life insured and the sub-variant selected.

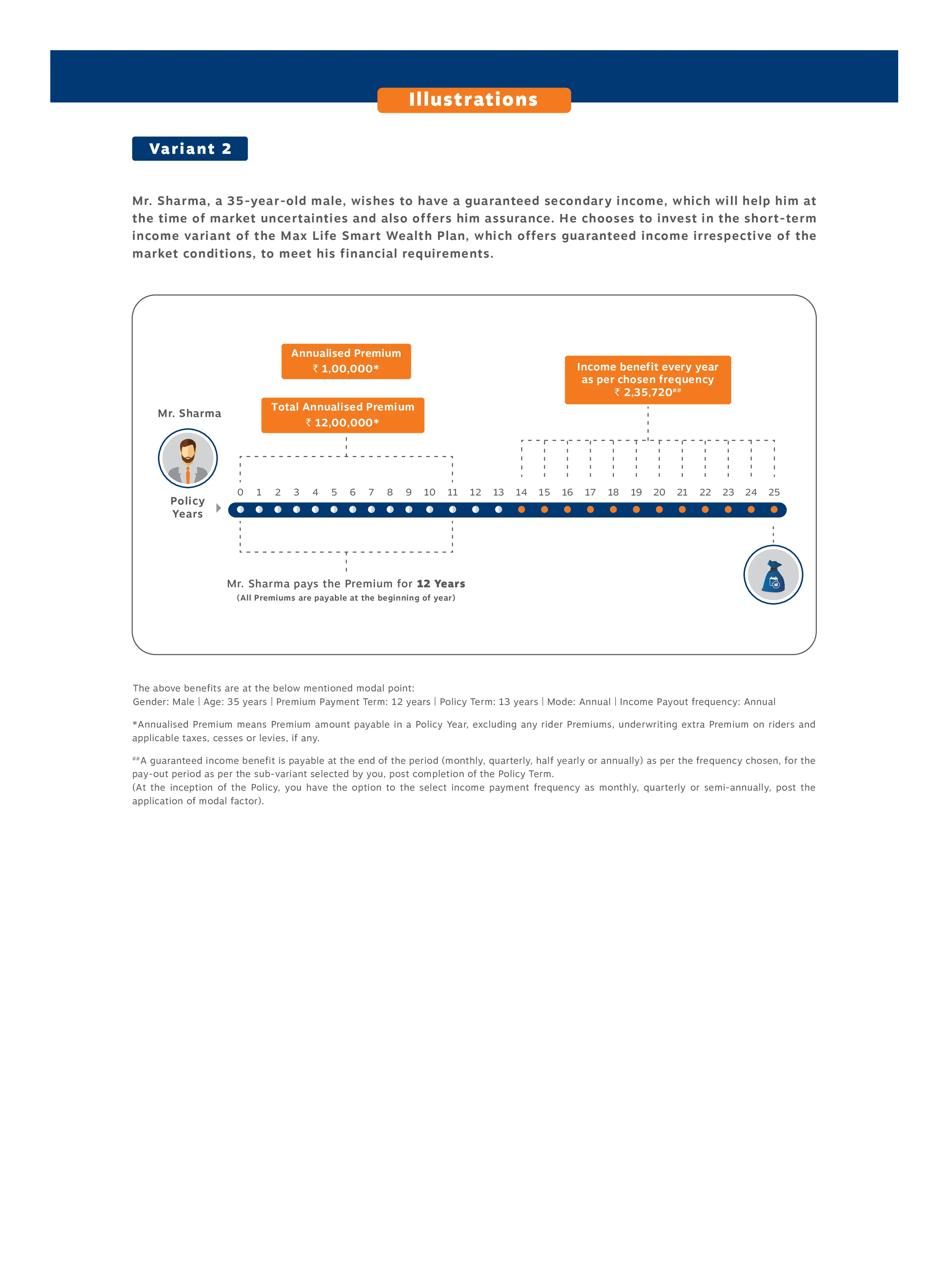

2) Short Term Income

This variant of Max Life Smart Wealth Plan offers to pay guaranteed ‘income benefit’ at the end of the period (monthly, quarterly, half yearly or annually) as per the frequency chosen, for the pay-out Period as per the sub-variant selected by you, post completion of the Policy Term. The income benefit is expressed as a percentage of the annualized premium. It varies by the entry age, premium band, and gender of the Life insured and the sub-variant selected.

3) Long Term Income

Under this variant, you receive a guaranteed ‘income benefit’ at the end of the period (monthly, quarterly, half yearly or annually) as per the frequency chosen, for the pay-out Period as per the sub-variant selected by you, post completion of the Policy Term. Moreover, after the pay-out period, you will also receive a ‘terminal benefit,’ which equals the Total Premiums Paid. Here, the income benefit is expressed as a percentage of annualized premium, and its value depends on the entry age, premium band, and gender of the Life insured and the sub-variant selected. Also, you can also choose the income pay-out frequency, other than annual.

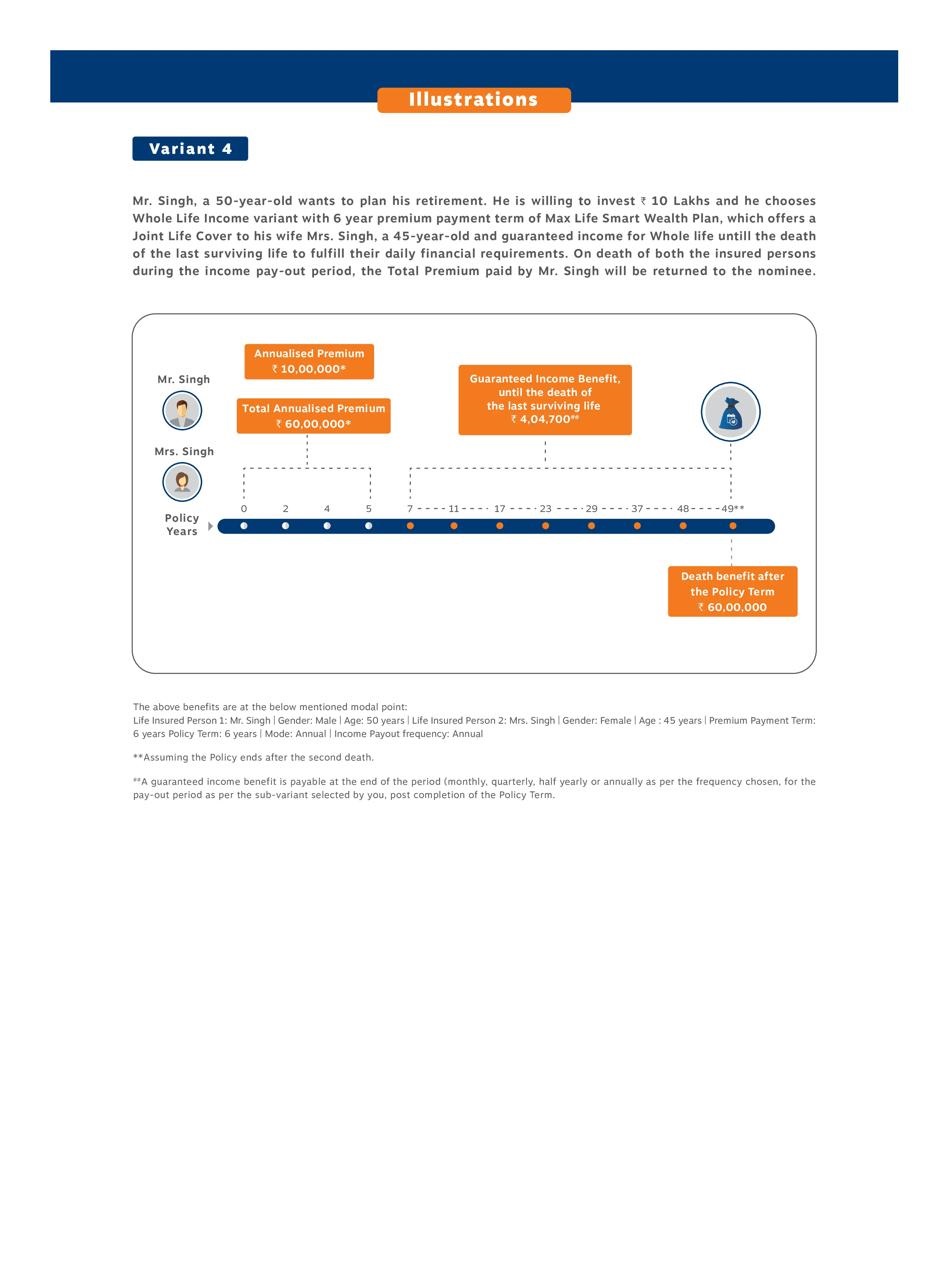

4) Whole Life Income

Under the Whole Life Income variant of Max Life Smart Wealth Plan, a guaranteed ‘income benefit’ is payable at the end of the period (monthly, quarterly, Half yearly or annually as per the frequency chosen, post the policy term, until the death of the last surviving life. Here, the income benefit is expressed as a percentage of the Single premium and varies by the entry age, gender, and premium band.

Step 2: Choose your Premium/Income Pay-out

Step 3: Choose your sub-variant, i.e. "Policy term and Premium payment term" from the available options

Variant | PPT | PT | Maturity Benefit | Single Life/Joint Life |

Lumpsum | 5 | 10,12,15,20 | Lump sum at the end of policy term | Single Life |

8 | 10,12,16,20 | |||

10 | 10,12,15,20 | |||

12 | 12,15,20 | |||

Short Term Income | 6 | 7 | Guaranteed income benefit for 6 years (from 8th year to 13th year in arrears) | |

8 | 9 | Guaranteed income benefit for 8 years (from 10th year to 17th year in arrears) | ||

10 | 11 | Guaranteed income benefit for 10 years (from 12th year to 21st year in arrears) | ||

12 | 13 | Guaranteed income benefit for 12 years (from 14th year to 25th year in arrears) | ||

Long Term Income

| 6 | 6 | Guaranteed income benefit for 25/30 years (from 7th year to 31st/36th year in arrears plus Terminal Benefit) | |

6 | 7 | Guaranteed income benefit for 30 years (from 8th year to 37th year in arrears plus Terminal Benefit) | ||

6 | 8 | Guaranteed income benefit for 25/30 years (from 9th year to 33rd/38th year in arrears plus Terminal Benefit) | ||

8 | 8 | Guaranteed income benefit for 25/30 years (from 9th year to 33rd/38th year in arrears plus Terminal Benefit) | ||

8 | 9 | Guaranteed income benefit for 25/30 years (from 10th year to 34th/39th year in arrears plus Terminal Benefit) | ||

8 | 10 | Guaranteed income benefit for 30 years (from 11th year to 40th year in arrears plus Terminal Benefit) | ||

10 | 10 | Guaranteed income benefit for 25/30 years (from 11th year to 35th/40th year in arrears plus Terminal Benefit) | ||

10 | 11 | Guaranteed income benefit for 25 years (from 12th year to 36th year in arrears plus Terminal Benefit) | ||

10 | 12 | Guaranteed income benefit for 25/30 years (from 13th year to 37th/42nd year in arrears plus Terminal Benefit) | ||

12 | 12 | Guaranteed income benefit for 25/30 years (from 13th year to 37th/42nd year in arrears plus Terminal Benefit) | ||

12 | 13 | Guaranteed income benefit for 25/30 years (from 14th year to 38th/43rd year in arrears plus Terminal Benefit) | ||

12 | 14 | Guaranteed income benefit for 25 years (from 15th year to 39th year in arrears plus Terminal Benefit) | ||

Whole Life Income | Single Pay | 5 | Guaranteed income benefit until the death of last survivor from 6th year in arrears | Joint Life |

6 | 6 | Guaranteed income benefit until the death of last survivor from 7th year in arrears |

What does Max Life Smart Wealth Plan has to offer?

Death Benefits

Variant 1, 2 and 3:

A lump sum guaranteed ‘Death Benefit’ is payable immediately on the death of the life insured during the policy term and is defined as higher of:

- 11 times the sum of Annualised Premium* and underwriting extra premiums***, (if any),

- 105% of all sum of Total Premiums Paid**, underwriting extra premiums*** and loadings for modal premiums, (if any) as on the date of death of life insured,

- Any absolute amount assured to be payable on death #

*“Annualised Premium” means Premium amount payable during a Policy Year chosen by Policyholder, excluding Underwriting Extra Premium, loading for modal premium, Rider Premiums and applicable taxes, cesses or levies if any;

**“Total Premiums Paid” means the total of all Premiums received, excluding Underwriting Extra Premium, loading for modal premium, Rider Premiums, and applicable taxes, cesses or levies, if any.

***“Underwriting Extra Premium” means an additional amount charged by Us, as per Underwriting Policy, which is determined on the basis of disclosures made by Policyholder in the Proposal Form or any other information received by Us including medical examination report of the Life Insured

#The absolute amount assured to be payable on death under these variants is equal to the Total Premiums Paid accumulated monthly at an interest rate of 8% p.a.

Variant 4:

A lump sum guaranteed ‘Death Benefit’ is payable immediately on the death of the life insured(s) during the term of the policy and is defined as the higher of:

- In case of Single Pay- 1.25 times the Single Premium* plus underwriting extra premiums (if any),

- In case of regular pay- 7 times the Annualised Premium* plus underwriting extra premiums (if any),

- 105% of sum of Total Premiums Paid**, underwriting extra premiums and loadings for modal premiums, (if any) as on the date of death of life insured,

- Any absolute amount assured to be payable on death #

*“Single Premium” means the lump sum premium amount paid by the policyholder at the inception of the policy excluding the taxes if any.

#The absolute amount assured to be payable on death under the Variant 4 on event of first death is equal to 1.25 times the Single Premium plus underwriting extra premiums (if any) in case of single pay and 7 times the Annualized Premium plus underwriting extra premiums (if any) in case of regular pay , and 10 times the Single Premium (Single Pay)/Annualised Premium (Regular pay) plus underwriting extra premiums (if any) on the event of the second death during the policy term.

The policy shall continue until the death of the last surviving policyholder.

On death of the last surviving policyholder post expiry of the policy Term, Single Premium plus underwriting extra premiums (if any) in case of single pay and total premiums paid plus underwriting extra premiums (if any) in case of regular pay shall be payable to the beneficiary.

The policy shall terminate on payment of the death benefit for the last surviving policyholder and no further benefits will be payable

Maturity Benefits

Variant 1:

On maturity the following benefit will be paid:

- Guaranteed Sum Assured on Maturity, plus

- Accrued Guaranteed Additions (if any).

The Guaranteed Sum Assured on Maturity for the variant is defined as follows:

Policy Term | Guaranteed Sum Assured on maturity |

10,12 | 110% x Annualised Premium x Premium Payment Term |

15,16 | 140% x Annualised Premium x Premium Payment Term |

20 | 160% x Annualised Premium x Premium Payment Term |

Guaranteed Additions is expressed as a percentage of annualised premium and varies by the entry age, premium band and gender of the life insured and the sub-variant selected.

Guaranteed additions accrue at the end of the last four policy years, provided the policy is either premium paying or fully paid up.

The Guaranteed Additions will be payable only in the event of maturity or surrender of the policy.

Variant 2:

A guaranteed “Income Benefit” is payable at the end of the period (monthly, quarterly, Half yearly or annually) as per the frequency chosen, for the pay-out Period as per the sub-variant selected by you, post completion of the Policy Term.

Income Benefit is expressed as a percentage of annualised premium and varies by the entry age, premium band and gender of the life insured and the sub-variant selected.

Variant 3:

A guaranteed “Income Benefit” is payable at the end of the period (monthly, quarterly, Half yearly or annually as per the frequency chosen , for the pay-out Period as per the sub-variant selected by you, post completion of the Policy Term. At the end of pay-out period a “Terminal Benefit” equal to the Total Premiums Paid, will be payable to the beneficiary.

Income Benefit is expressed as a percentage of Annualised premium and varies by the entry age, premium band and gender of the life insured and the sub-variant selected.

Variant 4:

Provided that, either of the two life insured have survived the policy term, a guaranteed “Income Benefit” is payable at the end of the period (monthly, quarterly, Half yearly or annually as per the frequency chosen , post the policy term, until the death of the last surviving life.

The policy shall terminate on payment of the death benefit for the last surviving life and no further benefits will be payable.

Income Benefit is expressed as a percentage of Single premium in case of Single pay and as a percentage of Annualized premium in case of regular pay and varies by the entry age, gender and premium band.

Eligibility Criteria

Eligibility Criteria | Plan Option | Minimum | Maximum | ||||||||||

Age at Entry (Years)* | Lumpsum | 0 (91 Days) | 65^^ | ||||||||||

Short Term Income | 5 | 65^^ | |||||||||||

Long Term Income | 4 | 65^^ | |||||||||||

Whole Life Income | Single Pay- 45 (Younger life) | 65 (Older Life) | |||||||||||

Regular pay- 40 (Younger Life) | 65 (Older Life) | ||||||||||||

^^Maximum age at entry to be calculated as 72 years less Premium paying term (subject to maximum entry age of 65 years ) | |||||||||||||

Age at Maturity (Years)* | Lumpsum | 18 | 85 | ||||||||||

Short Term Income | 18 | 73 | |||||||||||

Long Term Income | 18 | 74 | |||||||||||

Whole Life Income | 50 | 71 | |||||||||||

Minimum Premium# | Lumpsum | Annual: Rs. 11,000 | |||||||||||

Short Term Income | |||||||||||||

Long Term Income | |||||||||||||

Whole Life Income | Single Pay: Rs. 2,50,000 | ||||||||||||

Maximum Premium | All Options | No Limit, subject to Board Approved Underwriting Policy (BAUP) | |||||||||||

Premium Payment Mode & Modal Factors | Lumpsum | Annual, Semi Annual, Quarterly & Monthly

| |||||||||||

Short Term Income | |||||||||||||

Long Term Income | |||||||||||||

Whole Life Income | Single Premium & Regular Pay

| ||||||||||||

Gender | Male, Female and Transgender | ||||||||||||

Premium Rates/Benefits | Premium rates and benefits are uni-smoker. This plan can also be offered to sub standard lives with extra mortality charges subject to limits determined in accordance with the Board approved underwriting policy of the Company. | ||||||||||||

Eligibility Criteria | Variant | Policy Term | Entry Age (Minimum) | Entry Age (Maximum) |

Maximum age at entry* | Lumpsum | 10 | 8 | 55 |

12 | 6 | 53 | ||

15 | 3 | 50 | ||

16 | 2 | 49 | ||

20 | 91 days | 45 | ||

Short Term Income | 7 | 11 | 58 | |

9 | 9 | 56 | ||

11 | 7 | 54 | ||

13 | 5 | 52 | ||

Long Term Income | 6 | 12 | 59 | |

7 | 11 | 58 | ||

8 | 10 | 57 | ||

9 | 9 | 56 | ||

10 | 8 | 55 | ||

11 | 7 | 54 | ||

12 | 6 | 53 | ||

13 | 5 | 52 | ||

14 | 4 | 51 | ||

Whole Life Income | 6 | 40 (younger life) | 59 (Older life) | |

MMinimum and Maximum Age at Maturity* | 18 years and 65 years respectively | |||

Maximum Premium | Subject to 25 lakhs death benefit during the policy term | |||

Single pay in variant 4 of the product shall not be available for sales through POS persons

*All ages mentioned above are age as on last birthday

^^Maximum age at entry to be calculated as 72 years less Premium paying term (subject to maximum entry age of 65 years)

Please note- For policies sold through POS persons, the product shall comply with all the extant provision, rules, regulations, guidelines, circulars, directions, etc. applicable for POS products, as amended from time to time

How Do Max Life Smart Wealth Plan Variants Work?

Variant-1 (Lumpsum)

Variant-2 (Short Term Income)

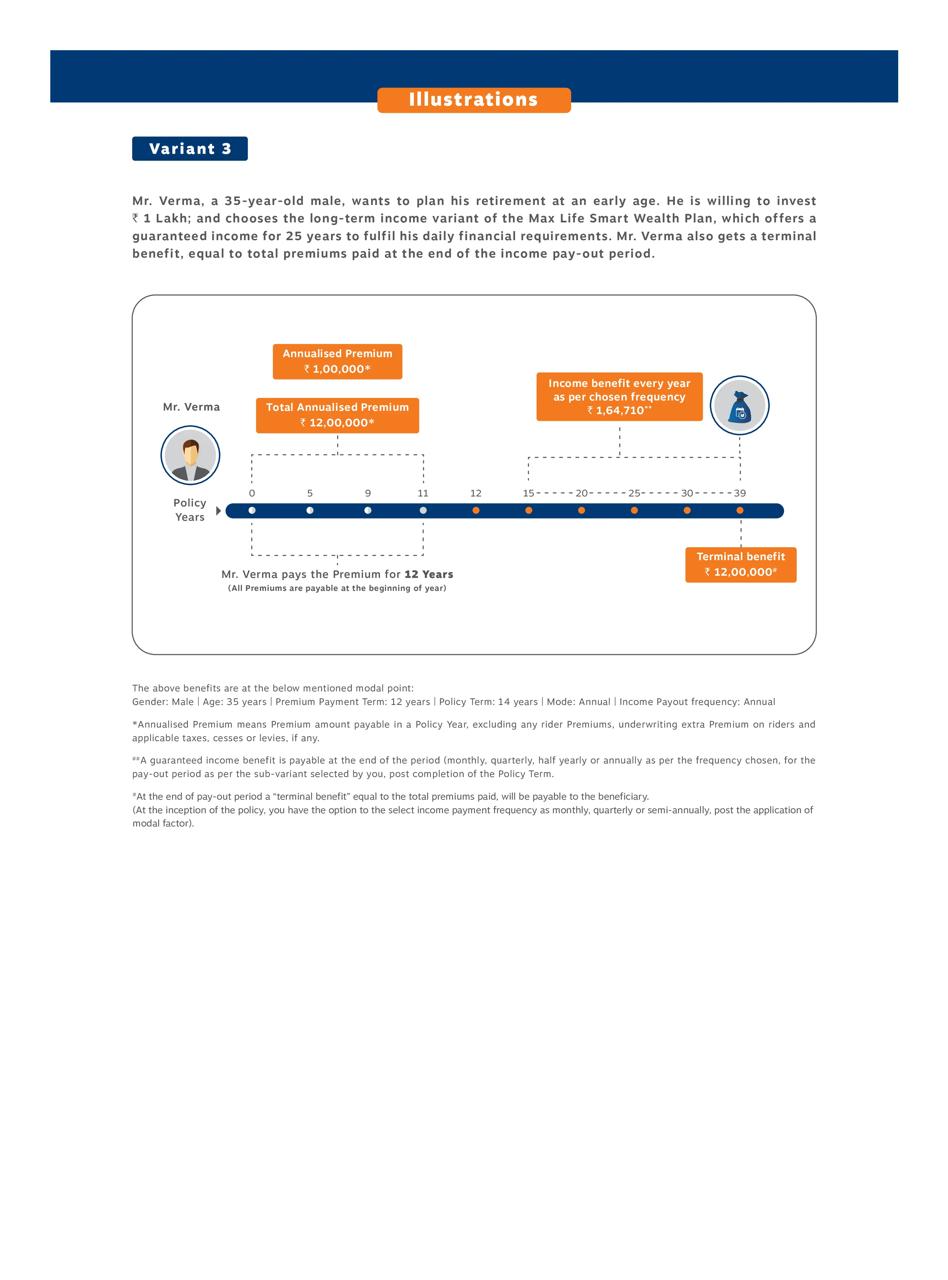

Variant-3 (Long Term Income)

Variant-4 (Whole Life Income)